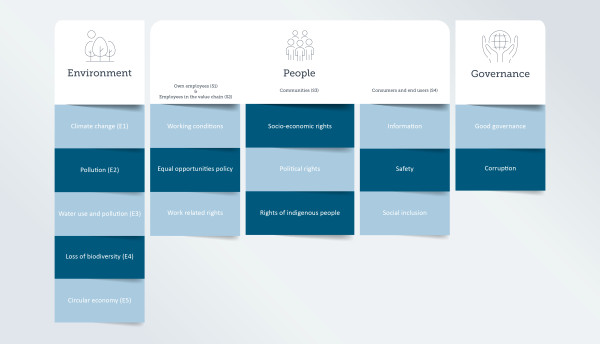

The CSRD is a new EU directive that will radically change the sustainability reporting of both large and small companies. This directive sets stricter reporting requirements, including a focus on double materiality. But what exactly is double materiality? In part 2 of our "Getting Started with CSRD" series, we tell you which sustainability topics your reporting should cover, and which reporting standards it should definitely meet.